Aug 2023

If you find this read interesting, share it on:

Robert Oppenheimer, the American theoretical physicist was not alone in admiring the Hindu text, the Bhagavad Gita. Henry David Thoreau wrote, "In the morning I bathe my intellect in the stupendous and cosmogonal philosophy of the Bhagavad Gita in comparison with which our modern world and its literature seem puny and trivial." Hermann Graf Keyserling, a German Philosopher regarded Bhagavad Gita as "Perhaps the most beautiful work of the literature of the world. Mahatma Gandhi was an ardent follower of the Bhagavad Gita. A. P. J. Abdul Kalam, the 11th President of India, used to read Bhagavad Gita and recite mantras. Sunita Williams, an American astronaut who holds the record for the longest single space flight by a woman who carried a copy of the Bhagavad Gita and Upanishads with her to space, said “Those are spiritual things to reflect upon yourself, life, the world around you and see things another way, I thought it was quite appropriate" while talking about her time in space.

As we start writing the Monthly Newsletter from a new perspective, we thought why not briefly discuss each chapter in the Bhagavad Gita (Gita). So, here’s an attempt, it’s subjective and we are not experts, we are also learning more as we write.

The first chapter of Bhagavad Gita says: The root cause of all sorrow and suffering in this world is our inability to deal with conflict. That is why the Gita was taught to Arjuna in the middle of a gruesome battlefield, with swords clanging, trumpets roaring and soldiers screaming. Conflict is everywhere, and we have to learn to handle it. The sooner we recognize this universal truth about conflict and its impact, the sooner we can progress in our personal, professional, and ultimately, spiritual journeys.

This is similar to what we experience in the markets perhaps most times with conflicting views and volatility and greed/ fear in the markets.

While it’s always best to invest at lower valuations. But over the longer term and investing in good companies has proven to give better returns than trying to time the markets or our investments.

As we write this monthly newsletter for August 2023, we often come across the conflict in the mind that is a good level to invest? Should we book profits and sit in Cash? Should we invest more? What should be the next step? As professional investors, what has worked for us over the years and you may have heard Alchemy’s Whole- Time Director & CIO, Hiren Ved say it many times is “underlying earnings and data”. So that’s what we do, we analyze the data available to us. Here are our thoughts/ analysis below on markets in July 2023 and underlying earnings momentum. This is after humbly accepting the fact that volatility is a constant in the financial markets and that’s a conflict one has to face.

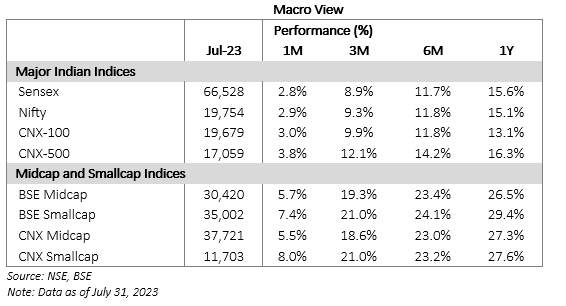

The tsunami of foreign portfolio funds to the Indian markets continues unabated. These inflows have led to the rapid conquest of Mount 19k by the Nifty and an assault on Mount 20k.

Nifty Index is up ~13% in FY24 as of July 31, 2023, with Midcaps and Smallcaps gaining ~22% and ~27% respectively during the same period. These returns have made us feel that markets have run up a lot.

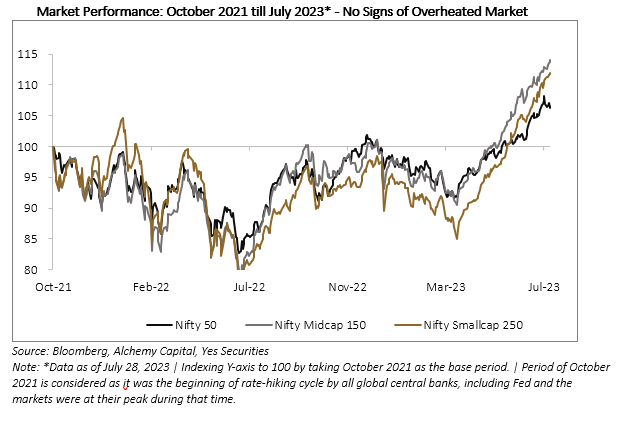

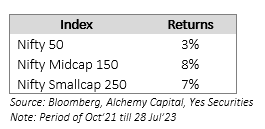

Let’s broaden our horizons a little more. The markets peaked around mid-October 2021. Since then, the CAGR return in Nifty is about 3%, Midcap about 8%, and Smallcap about 7%. These numbers do not reflect an overheated market, especially considering double-digit earnings growth.

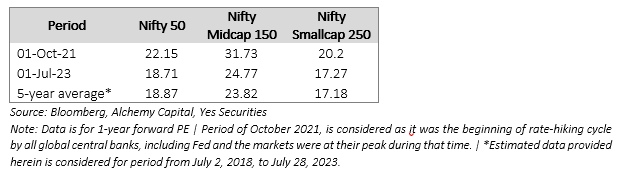

In mid-October 2021, Nifty 1yr fwd P/E was ~22x, whereas in July 2023, it is ~18.7x (close to 17% lower) and it is at same levels as of 5-year average. Similarly, Nifty Midcap 150 Index’s 1yr fwd P/E has corrected by ~30% to ~24.7x and Nifty Smallcap 250 Index’s 1yr fwd P/E to ~17.3x mostly on account of earnings growth.

With inflation showing signs of moderation, we may likely be closer to the end of the rate hike cycle than the beginning. US Inflation has corrected from multi decade high of 9.1% to 3% as of June 2023, quite close to the 2% target of the Federal Reserve.

Back in India too, CPI inflation has come down sharply from 9-year highs of 7.8% to 4.8% as of July 2023, well within RBI tolerance bands.

This is fuelling optimism about the Federal Reserve being closer to the end of the rate hike cycle. This combined with global GDP growth being still positive, is raising expectations of a soft landing.

The ongoing Quantitative Tightening (QT) however ensures that there is no longer any easy money and thus profitability is as important as Topline/Sales/GMV. It’s the right stock picking that would be rewarding.

Some Interesting Nuggets on Sectors

Takeaways for Rural Consumption: Hindustan Unilever’s continued to underperform due to its disappointing June 2023 quarter results. But a silver lining from its management commentary, not just for the company but for the industry and even the country, is a nascent recovery in India’s rural FMCG sales growth. It rose in the June 2023 quarter by around 2%, after declining in all of FY23. While this growth may be partly due to a low base effect, as the year-ago quarter saw a decline, it’s still better than if the decline had continued unabated.

It raises the prospect of whether FY24 could be the year of a rural recovery, for the FMCG sector surely but for other consumer sectors as well.

Public sector banks, the battered lot during the better part of the last decade, like Barbies, were the flavour of the season. Over a period of one year, the PSU Bank index has outperformed. This is not without reason, but perhaps it is without restraint.

We believe that the multiple re-ratings of PSU bank shares have been driven by the improvement in asset quality. The argument is that PSU bank valuations have been decimated and their asset quality improvement makes them great bargain picks for investors. That said, PSU Bank’s net profit growth and loan growth do not overshadow its historic trend. Granted, quarterly net profit for some PSU banks more than doubled but a lot of it is on account of a drop in provisions, also loan growth has lagged private peers. Even the gross bad loan ratio is way above private sector peers. We must keep in mind that banks did not improve their asset quality metrics entirely by getting their money (loan amount) back. Write-offs and haircuts also have a large share. We want to make sure that structural change takes place.

If we look at a couple of stocks in our portfolio this month:

One stock that raised our expectations like Mission Impossible and then fell off the cliff has been Eicher Motors, we were very confident that Eicher Motors amongst the leading player in the 2W space with its Royal Enfield (RE) motorcycles having ~ 90%+ market share in the Indian mid-size segment, two iconic brands- Classic and Bullet. They had also added more products which were doing well such as Hunter which appealed to a younger audience.

Bajaj and Hero announced new product launches aimed at this segment with a 10-15% premium over the best selling RE bike. We believe that the competition will affect growth for RE from FY25 as the two peers ramp. How much impact it has is something only time would be able to predict, but from being a monopolistic market it is becoming more competitive. As a result, we had to exit the stock for now.

Among Nifty stocks, buybacks were dominated by IT companies. It is, therefore, a pleasant surprise to see infrastructure and engineering giant L&T announced an INR 10,000 crore buyback. In 2019, L&T announced a buyback worth INR 9,000 crore, but this was rejected by SEBI on the ground of its high debt position at the consolidated level. Since then, the company has improved its financials, reduced its debt-to-equity ratio and exited non-core businesses. L&T’s buyback sends a message that not only IT companies but other firms in the manufacturing sector are also enjoying strong cash flow generation.

Another company that was the focus last month has been Tata Motors backed by new products, and strong demand, the company was able to register a 29% year-on-year (YoY) growth in volumes. Its revenues, however, registered a much higher growth of 57% YoY, thanks to the higher realisation on the back of a new product range.

Higher revenue and the softening of raw material prices led JLR to post an EBITDA (earnings before interest, tax, depreciation, and amortisation) margin above 16% which in our view is a commendable performance. The margin expanded by a whopping 960 basis points on a YoY basis.

The company has proposed a scheme of cancellation of DVR shares by offering 7 ordinary shares for every 10 DVR share held by the shareholders; this translated into a ~20% premium to the existing DVR price. Also, this transaction will reduce the total share capital by 4%, making it EPS accretive for all shareholders.

Back to Arjuna’s dilemma and the first chapter in the Bhagavad Gita. When confronting the material conflict of battle, Arjuna’s rational mind was clear – he was a warrior, and he had entered the battlefield to fight a war against the enemy for a just cause. But eventually his ego – the primitive side of his mind – took control away from his rational mind. It went into “flight” mode. It made him say, it is better to run away and become a monk, than to perform my duty. The inability to reconcile this conflict in his mind led to his mental breakdown in the middle of the battlefield. He could not commit to fighting, and being unable to decide, he wanted to quit

So then, conflict at the material level, and at the mental level, is pervasive. It is an integral part of life. We cannot escape it. But so what? Shouldn’t we just accept this state of affairs?

Himani Shah

SVP - Investments & Research

Alchemy Capital Management Pvt. Ltd.