Mar 2023

If you find this read interesting, share it on:

We see a bottom-up market in India over the next 2-3 quarters with no clear direction for the broader market and not too many sectoral themes playing out. Our focus remains, therefore on individual companies as we expect divergent performance even within sectors. The only over-arching trend, in our opinion, is that quality companies will make a comeback. Even within that subset, we expect ultra-expensive stocks to remain challenged given the macro challenges on inflation and interest rates.

We see this as a temporary blip in a strong longer-term India story. The tailwinds for India still remain robust – rising per capita income, increasing digitisation, the comeback in manufacturing and financial system stability. In that context, investors should keep their strategic exposure to equities fully allocated. Tactical positions in equities could, however, be measured; and lumpsums should be invested in a staggered manner.

3Q Results: Margin Pressures Continue

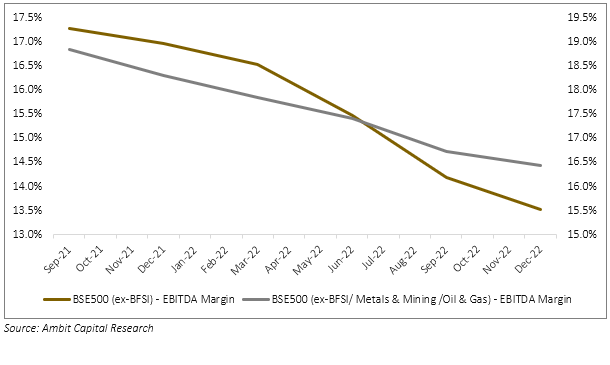

The 3QFY23 results were a continuation of recent trends and there were no substantial inflexion points. The overarching theme was that growth was robust, aided by inflation, but margins remained challenged. The key takeaways are:

- Top line growth remained robust at ~20% (BSE-500, ex financials) though we believe that there was a significant impact of inflation. Volume growth for consumer companies was disappointing, especially for those that are exposed to the mass market. We believe that this is a cyclical headwind and should recover over the next 3-4 quarters, driven by declining inflation, improved stability in household finances after the Covid shock and improved infra spending.

- There was little relief in aggregate margins – though the continuous fall seems to have been arrested. We are more optimistic about margins for CY22 as commodity prices stabilise and companies start to pass on price hikes to the consumers. We, however, do not expect margins to touch previous peaks in the next 2-3 quarters as the damage has been significant.

- In our view, one bright spot was the auto sector, which reported strong revenue growth and a margin bounce back. The sector is coming out of a multi-year winter of weak demand, cost pressures, and supply chain challenges. We see a long runway of growth and premiumisation trends across both 2- and 4-wheelers.

Sectoral Outlook

We start a new segment in our monthly update where we present views on major sectors. We shall revisit these once every few months.

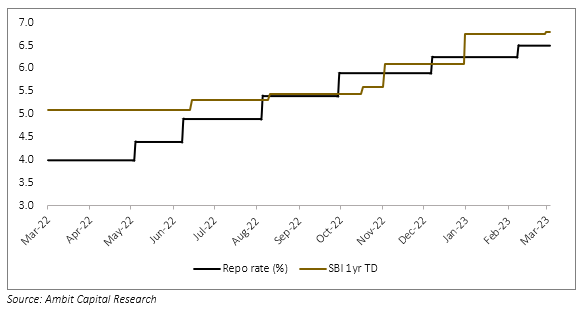

Financials

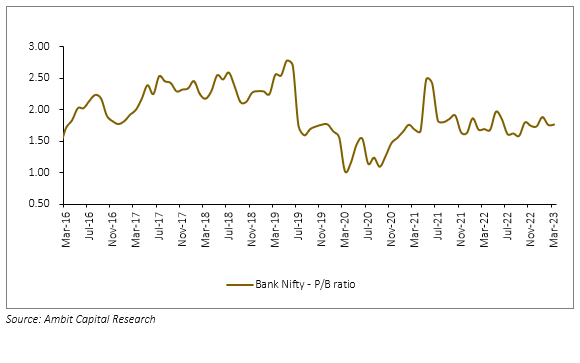

- Net interest margins for banks are close to their peak. The sector benefited from the upswing in policy rates that drove loan yields up in tandem. The trend is reversing now as deposit costs are catching up and policy rates are close to the peak. The exception is banks with low exposure to mortgages, which should be resilient on NIMs. For NBFCs, the cycle now reverses – their cost of funds spiked in 2022 and loan yields (which are mostly fixed) should now catch up.

- The sector has now harvested most of the post-covid asset quality benefits. Credit costs are unlikely to shrink further, though they should stay “lower for longer” – ie, we think the benign cycle is here to stay. Asset quality, however, is unlikely to be a driver for improving ROAs from here.

- We see no sector re-rating triggers for financials as a whole, unlike in CY22. Sector fundamentals will be mixed – slowing loan growth, volatile NIMs and no clear levers on costs. We are looking at the sector at a company level – looking for individual drivers of relating and stock price. We see many banks and NBFCs coming out of a multi-year stress period and could be ripe for re-rating. The key factors we look at are NIM outlook, market share gains, and relative valuations.

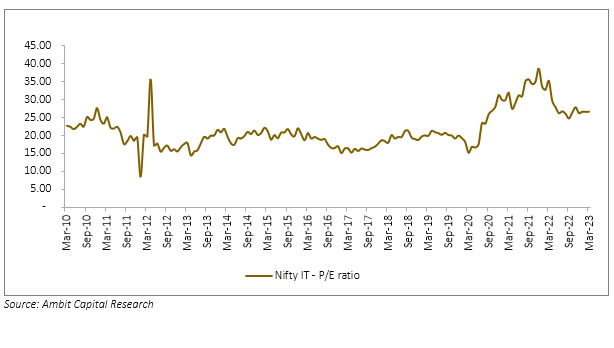

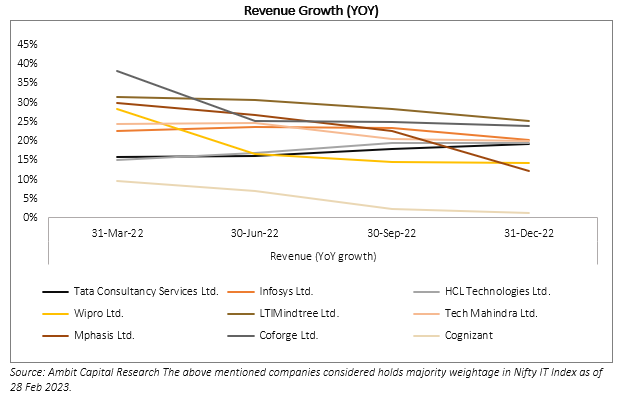

Information Technology

The sector has been significantly de-rated in 2022 due to stretched valuations, growth worries and margin pressures from rising wage costs. All three have now reversed in various degrees.

- Revenue growth appears to be resilient, with management commentary indicating that the hit may not be as significant as earlier thought. The relatively benign slowdown in the US and the need for clients to keep investing in transformative technology appear to be the drivers. We do believe that growth will slow in FY24, but that is largely discounted.

- The margin outlook for the sector is benign. Wage cost pressures are easing – from lower bench strength, muted salary hikes and a drop in subcontracting.

- Valuations are relatively undemanding. The post-Covid demand surge had been extrapolated to be structural – which led to frothy valuations. As the risks emerged, there was a savage derating and stocks are now reasonably valued.

- The sector looks attractive from the medium term, but short-term challenges do persist. Also, we see smaller companies remaining a little more vulnerable. Here again, we would be selective in picking stocks based on growth resilience, scale and valuations.

Consumer

- The consumer sector continues to face headwinds on overall demand. The exception is premium goods where the demand has been very strong since COVID those some of that is now seeing a base effect. On the other hand mass consumption demand continues to be challenged and volume growth in those segments remains weak in 3rd quarter. The key problem appears to be inflation which is constricting household budgets. The problem is accelerated by FMCG companies being forced to take price hikes due to rising input costs.

- The good news is that inflationary pressures are probably easing as a high base effect kicks in. If employment remains buoyant then we believe that consumers will adjust to the new prices and demand should start to come back over CY23.

- Valuation is a key issue for the consumer sector why this while this sector deservedly commands a premium the relative valuations had expanded to unsustainable levels because of a scarcity factor. However, post COVID the pool of quality companies with strong balance sheets comfortable cash generation and rising return ratios has expanded which we believe will affect the relative valuations of the sector.

Manufacturing

The manufacturing sector has strong demand tailwinds from a revival in domestic capex (both state and central) and Global supply chain diversification. This is visible not only from macro trends like government spending but also from anecdotal evidence of companies strong order books. We, therefore, see a long runway of growth for the sector which includes capital goods auto ancillaries chemicals and pharma intermediates.

The sector also benefits from a survivor bias. The companies that survived the stresses of the decade 2010 to 2020 are almost by definition lean and efficient which strong balance sheets. They are therefore in a position to capitalise on this multi year upsurge in demand. In the short term, there may be some margin pressures due to high commodity prices. Some of these have already been visible and we think that the normalization of margins may take a little more time.

The challenge for the sector is that valuations in many cases have stretch to unsustainable levels. While the macro story for this sector remains positive, we believe that a broad sector rally from these levels is unlikely. Even for such a “hot” sector, we prefer being selective about which stocks we own with one eye on valuations. We have to be especially cautious about this for manufacturing companies as valuations for B2B companies tend to get capped out.

Seshadri Sen

Head of Research

Alchemy Capital Management Pvt. Ltd.